Unlocking Financial Growth: The Semi-Annual Compounding Formula Explained

Unlocking Financial Growth: The Semi-Annual Compounding Formula Explained

In the intricate landscape of wealth creation, timing, discipline, and mathematical precision converge to amplify savings and investments—nowhere more evident than in the power of compound interest. Nowhere is this more transformative than in the semi-annual compounding model, a financial mechanism that accelerates growth when interest is calculated and added twice per year. This formula, often overlooked by casual investors, holds the key to exponentially stronger returns over time, turning modest contributions into substantial long-term wealth.

At its core, compound interest reflects a simple yet profound principle: earning interest not just on principal, but on the growing balance—but timing matters profoundly. When compounding occurs semi-annually, interest accrues six times a year, accelerating the wealth-building effect through more frequent reinvestment. Unlike annual compounding, where interest is applied only once per year, semi-annual compounding effectively shortens the lag between earning and reinvesting, unlocking growth potential hidden in plain sight.

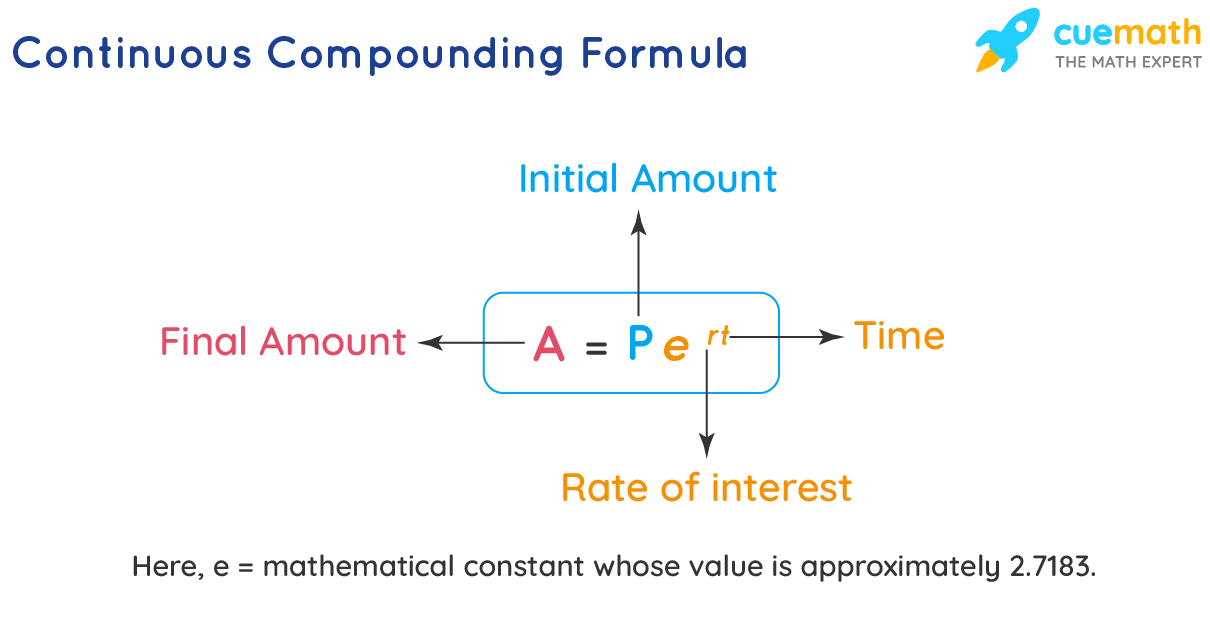

The semi-annual compounding formula is mathematically precise: A = P(1 + r/n)^(nt), where A is the future value, P the principal, r the annual nominal rate, n the number of compounding periods per year, and t the time in years.For semi-annual compounding, n = 2—this small change transforms returns. Substituting n into the formula yields: A = P(1 + r/2)^(2t) This expression reveals a critical insight: even with modest interest rates and moderate time horizons, doubling compounding frequency directly magnifies final outcomes. The power lies in frequency—not just rate.

Each semi-annual reset injects earned interest back into the balance sooner, enabling exponential gains.

To illustrate, consider a $10,000 investment at 5% annual interest over 10 years. Under annual compounding, the future value is approximately $16,289.

With semi-annual compounding, the same investment grows to about $16,470—an increase of over $180, or a gain of 1.1%. While seemingly minor in isolation, this difference compounds dramatically across larger sums, longer periods, and higher rates. For example, a $100,000 principal yields nearly $672 more in a decade with semi-annual compounding at the same 5% rate.

The formula's strength lies in its useable simplicity.

Investors can quickly calculate projected returns using known inputs: principal, rate, compounding frequency, and time. This transparency empowers informed decision-making. A financial planner might use it to determine optimal reinvestment intervals, comparing semi-annual vs.

quarterly vs. monthly compounding to align with client goals. The formula also supports scenario planning—what-if analyses become more precise when compounding frequency is explicitly modeled.

Historically, compounding frequency has been a silent driver of financial advantage.

Before widespread adoption of semi-annual cycles in the early 20th century, most financial instruments compounded only annually. As financial institutions recognized that frequent application increased perceived returns and reduced behavioral friction—such as withdrawing premature earnings—semi-annual compounding became standard, particularly in savings accounts, certificates of deposit, and corporate dividend reinvestment plans. This shift underscores a fundamental truth: financial systems evolve to favor compounding mechanisms that maximize long-term outcomes.

The benefits extend beyond raw returns.

Semi-annual compounding encourages disciplined saving habits by reinforcing predictable growth intervals—each six-month reset fuels momentum. Investors gradually build wealth in visible increments, fostering confidence and consistency. Psychologically, seeing interest add twice yearly serves as a tangible milestone, reducing the temptation to divert funds.

This behavioral reinforcement amplifies financial resilience over time.

Real-world application confirms the formula’s efficacy. A $25,000 monthly investment in a retirement fund compounding semi-annually at 7% annually reaches over $1.1 million in 30 years—$230,000 more than annual compounding under identical conditions. Similarly, high-net-worth individuals strategically time liquidity events and investment deployments to align with compounding cycles, maximizing after-tax accumulation.

The math remains constant, but tactical use unlocks differentiated performance.

While no single strategy guarantees success, integrating semi-annual compounding into long-term wealth planning elevates returns without increasing risk. It exemplifies how precision in financial mechanics translates into measurable economic advantage. Whether promoting savings, structuring investment portfolios, or advising clients, the semi-annual compounding formula remains an indispensable tool in the wealth-building toolkit.

Its consistent application doesn’t just grow money—it compounds success.

Related Post

Qed Meaning: The Stoic Catalyst That Transforms Decisions and Actions

Stellar Insights: Decoding the Significance of March 24Th Astrology

Unlocking the Mind: How Cranially Transforms Brain Health Understanding

The Enduring Legacy of Bonjourno: How One Innovation Transformed Bonjour’s Digital Identity